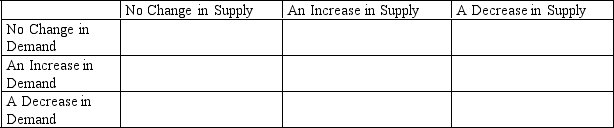

Fill in the accompanying table, showing whether equilibrium price and equilibrium quantity go up, down or stay the same.

Definitions:

Marginal Cost

The elevation in costs incurred by the creation of an additional unit of a good or service.

Long-Run Equilibrium

A state in which all factors of production and economic inputs can be fully adjusted, and all market forces are balanced.

Increase in Demand

A situation where the quantity of a good or service that consumers are willing and able to purchase at a particular price rises.

Marginal Revenue

The additional revenue that a firm gains when it sells one more unit of a product or service.

Q4: Which of the following best describes the

Q13: If a country's saving rate increases, which

Q32: One of the Ten Principles of Economics

Q45: Which of the following is the source

Q74: If a small country has current nominal

Q76: Suppose that Carolyn receives a pay increase.

Q125: If cigarettes and marijuana had been found

Q162: Which of the following best describes nominal

Q194: Market demand is given as Qd =

Q265: What is an example of a perfectly