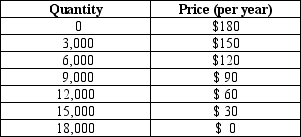

Table 17-3. The information in the table below shows the total demand for premium-channel digital cable TV subscriptions in a small urban market. Assume that each digital cable TV operator pays a fixed cost of $200,000 (per year) to provide premium digital channels in the market area and that the marginal cost of providing the premium channel service to a household is zero.

-Refer to Table 17-3.Assume there are two profit-maximizing digital cable TV companies operating in this market.Further assume that they are not able to collude on the price and quantity of premium digital channel subscriptions to sell.How many premium digital channel cable TV subscriptions will be sold altogether when this market reaches a Nash equilibrium?

Definitions:

Hybrid Automobile

A vehicle that uses two or more distinct types of power, such as an internal combustion engine plus an electric motor, to achieve better fuel efficiency and lower emissions than conventional vehicles.

Market for Gasoline

The supply and demand interaction for gasoline, determining its price in the market.

Equilibrium Price

Equilibrium price is the price at which the quantity of goods demanded by consumers matches the quantity of goods supplied by producers, resulting in a market balance where there is neither excess supply nor excess demand.

Chocolate Consumption

Refers to the amount and frequency at which chocolate is consumed by individuals or populations, indicating preferences and economic spending on confectionery.

Q85: One key difference between an oligopoly market

Q89: Refer to Figure 16-1.The firm's profit-maximizing level

Q117: Acme Computer Co.sells computers to retail stores

Q122: For cartels,as the number of firms (members

Q187: Refer to Figure 16-4.Which of the graphs

Q203: Which of these situations produces the largest

Q210: A central issue in the Microsoft antitrust

Q248: Suppose three firms form a cartel and

Q312: In the language of game theory,a situation

Q338: Along the vertical axis of the production