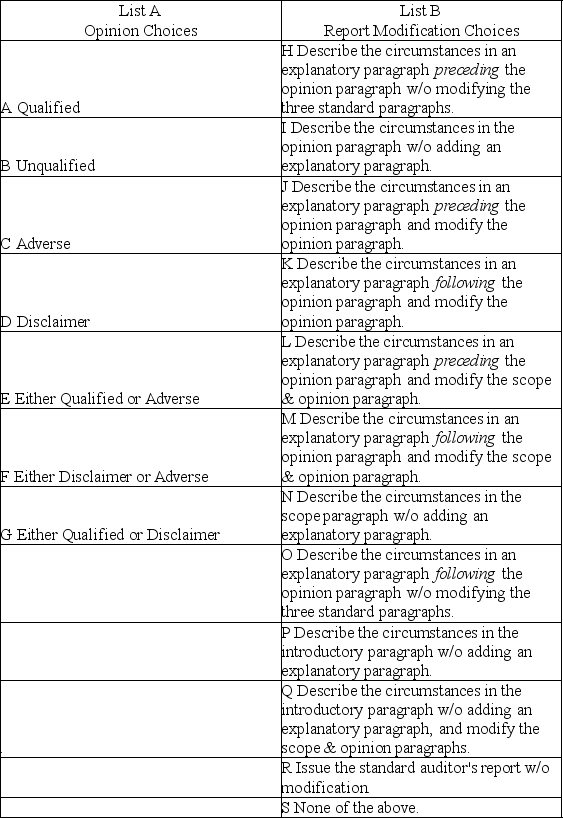

Audit situations 1 through 10 present various independent factual situations an auditor might encounter in conducting an audit.List A represents the types of opinions the auditor ordinarily would issue,and List B represents the report modifications (if any)that would be necessary.For each situation,select one response from List A and one from List B.Select,as the best answer for each item,the action the auditor normally would take.Items from either list may be selected once,more than once,or not at all.

Assume the following:

• The auditor is independent

• The auditor previously expressed an unqualified opinion on the prior-year financial statements unless otherwise noted

• Only single-year (not comparative)statements are presented for the current year (unless otherwise stated)

• The conditions for an unqualified opinion exist unless contradicted in the factual scenario

• The conditions stated in the factual scenario are material

• No report modifications are to be made except in response to the factual scenario

Factual Scenario

1.The financial statements present fairly,in all material respects,the financial position,results of operations,and cash flows in conformity with GAAP.

2.In auditing the Long-Term Investments account,an auditor is unable to obtain audited F/S for an investee located in a foreign country.The auditor concludes that sufficient competent evidential matter regarding this investment cannot be obtained but it is not pervasive to the financials as a whole.

3.Due to recurring operating losses and working capital deficiencies the auditor has substantial doubt about an entity's ability to continue as a going concern for a reasonable period of time.However,the F/S disclosures are adequate.

4.The principal auditor decides to refer to the work of another auditor,who audited a wholly owned subsidiary of the entity and issued an unqualified opinion.

5.An entity issues F/S that present financial position and results of operations but omits the related statement of cash flows.Management discloses in the notes to the F/S that it does not believe the statement of cash flows to be useful.

6.An entity changes its depreciation method for production equipment from SL to units of production based on hours of utilization.The auditor concurs with the change,although it has a material effect on the comparability of the entity's F/S.

7.An entity is a defendant in a lawsuit alleging infringement of certain patent rights.However,management.cannot reasonably estimate the ultimate outcome of the litigation.The auditor believes that there is a reasonable possibility of a significant material loss,but the lawsuit is adequately disclosed in the notes to the F/S.

8.An entity discloses certain lease obligations in the notes to the F/S.The auditor believes that the failure to capitalize these leases is a departure from GAAP.

9.The entity wishes to show comparative F/S and include the prior year.However,the prior year F/S contained a qualification due to an inappropriate method of GAAP.Accordingly,management.corrected the prior year GAAP deficiency and included the updated numbers in the comparative financials for the current year.

10.The entity wishes to show comparative F/S and include the prior year.However,the prior year F/S were audited by another auditor who refuses to reissue his opinion.

Definitions:

Duty to Be Careful

An obligation to act with a reasonable level of care and caution to avoid harm to others or their property.

Business Interruption

An event that causes significant disruption to the normal operations of a business, potentially leading to financial loss.

Tort

A wrongful act or infringement of a right leading to civil legal liability, not arising from a contract.

Umbrella Insurance

A type of extra liability insurance that provides additional coverage beyond the limits of the insured's homeowners, auto, or watercraft insurance policies.

Q11: Explain each of these terms: antibiotic,antibody,antigen,antihistamine,antiretroviral drug,antiviral

Q24: Privity of contract exists between:<br>A) auditor and

Q30: One of the AICPA's Ethical Principles deals

Q34: Discuss the differences in the auditor's responsibilities

Q48: The PCAOB considers International Standards on Auditing

Q55: A member in public practice shall neither

Q65: When an auditor believes that an illegal

Q68: The auditor's responsibility section of the standard

Q100: The Sarbanes-Oxley Act requires the CEO and

Q109: In the condition known as cryptorchidism,<br>A) the