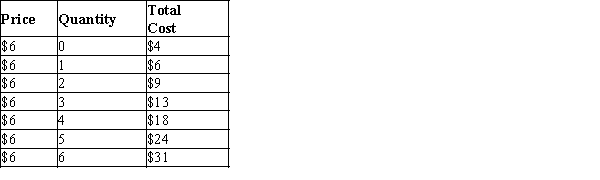

Table 14-11

Suppose that a firm in a competitive market faces the following prices and costs:

-Refer to Table 14-11. The marginal revenue from producing the 3rd unit equals (i) $6.

(ii) the price.(iii) the marginal cost.

Definitions:

Standard Quantity

This term refers to the amount of input (materials, labor, etc.) that should be used in the production of a unit of goods under normal conditions.

Standard Price

A pre-determined cost allocated to a single unit of product or service, used for budgeting and performance evaluation.

Ideal Standards

Standards that assume peak efficiency at all times.

Materials Quantity Variance

The difference between the actual quantity of materials used in production and the expected (standard) quantity, multiplied by the standard cost of those materials.

Q7: When firms in a competitive market have

Q57: Refer to Figure 13-1. Which of the

Q64: Consider a small hair styling salon. List

Q130: When firms are neither entering nor exiting

Q155: The nature of a firm's cost (fixed

Q309: Because of the greater flexibility that firms

Q339: What effect, if any, does diminishing marginal

Q366: Jacqui decides to open her own business

Q381: For a firm operating in a competitive

Q411: Marginal costs are costs that do not