Figure 13-2

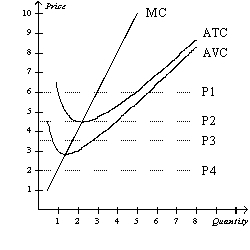

Suppose a firm operating in a competitive market has the following cost curves:

-Refer to Figure 13-2.If the market price is P1,in the short run the firm will earn

Definitions:

Production Technology

The set of processes, methods, or equipment used by firms in the production of goods or services, which affects productivity and efficiency.

Input Prices

The cost of raw materials and other inputs used in the production of goods and services. Lower input prices can increase profitability for producers.

Production Technology

The methods, processes, and equipment used to produce goods and services.

Input Prices

The costs associated with the inputs required for production, including materials, labor, and overhead expenses.

Q25: Refer to Table 14-8.What is the additional

Q27: Marginal cost increases as the quantity of

Q30: A monopolist will choose to increase output

Q169: When new entrants into a competitive market

Q229: If identical firms that remain in a

Q246: In the long run,a profit-maximizing firm will

Q317: If a firm experiences constant returns to

Q466: Refer to Scenario 14-3.At Q = 500,the

Q475: Refer to Table 13-8.The firm will produce

Q522: Suppose a monopolist charges a price of