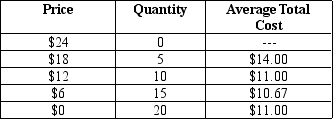

Table 14-8

The following table provides information on the price,quantity,and average total cost for a monopoly.

-Refer to Table 14-8.What is the maximum profit that the monopolist can earn?

Definitions:

Short Run

In economics, a period in which at least one input, such as plant size, cannot be changed; distinct from the long run where all inputs can be varied.

Long Run

A period in economics during which all factors of production and costs are variable, allowing for full adjustment to changes.

Perfectly Elastic

Describes a situation where the quantity demanded or supplied changes by an unlimited amount in response to any change in price.

Competitive Firm

A business that operates in a market with many buyers and sellers, where the company does not have the market power to set prices.

Q92: A dairy farmer must be able to

Q120: For a firm operating in a perfectly

Q261: Refer to Table 14-18.If the monopolist can

Q285: Refer to Figure 13-2.Which of the four

Q324: A profit-maximizing firm in a competitive market

Q334: Which of the following statements is correct

Q401: Monopolists can achieve any level of profit

Q408: In a simple circular-flow diagram,firms use the

Q414: If the price of a Blu-Ray Disc

Q486: For a monopolist,when the output effect is