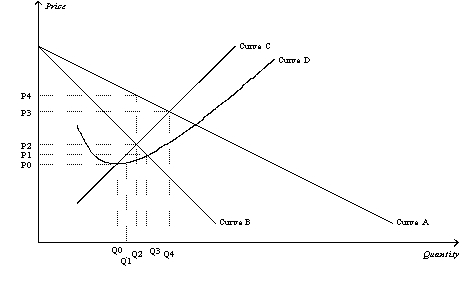

Figure 14-3

-Refer to Figure 14-3.The average total cost curve for a monopoly firm is depicted by curve

Definitions:

Constant-Cost Industry

An industry in which the input costs do not change significantly with changes in output levels, often resulting in stable product prices over time.

Long-Run Equilibrium

A state in which all factors of production and variables in a market are in balance over a longer period, with no external pressures prompting change.

Decrease in Demand

A downward shift in the demand curve, indicating that consumers are willing to purchase less of a good or service at each price point.

Resource Prices

Refers to the costs associated with inputs used in the production of goods or services, such as raw materials, labor, and capital.

Q146: According to the circular-flow diagram GDP<br>A) can

Q172: The supply curve of a firm in

Q174: The basic tools of supply and demand

Q218: Refer to Figure 13-2.If the market price

Q241: The DeBeers company faces very little competition

Q269: Bill operates a boat rental business in

Q340: A firm that is a natural monopoly<br>A)

Q350: In the long run,when price is greater

Q426: Refer to Table 13-11.The marginal revenue from

Q460: A patent gives a single person or