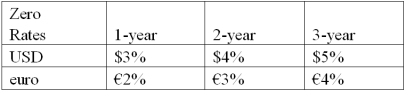

Suppose that you are a swap bank and you notice that interest rates on zero coupon bonds are as shown.Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR.  In other words,what will you be willing to pay in euro against receiving USD LIBOR?

In other words,what will you be willing to pay in euro against receiving USD LIBOR?

Definitions:

Kruskal-Wallis Test

A nonparametric statistical test used to determine if there are statistically significant differences between two or more groups of an independent variable.

Chi-Squared Distribution

A statistical distribution employed in hypothesis testing that is known for its utility in evaluating the goodness-of-fit between observed and expected data.

Sample Sizes

Refers to the number of observations or elements chosen from a population to form a sample for a statistical study.

Kruskal-Wallis Test

A non-parametric test used to determine if there are statistically significant differences between two or more groups of an independent variable on a continuous or ordinal dependent variable.

Q8: Advantages of investing in mutual funds known

Q15: Which of the following would be an

Q37: Eurocredits feature rollover pricing.<br>A)Rollover pricing was created

Q38: Teltrex International can borrow $3,000,000 at LIBOR

Q41: Find the debt-to-value ratio for a firm

Q48: A 5%-annual coupon British has a par

Q65: Compute the payments due in the second

Q74: Severe imperfections in the labor market lead

Q91: Transfer risk refers to the risk which

Q92: Banks that both perform traditional commercial banking