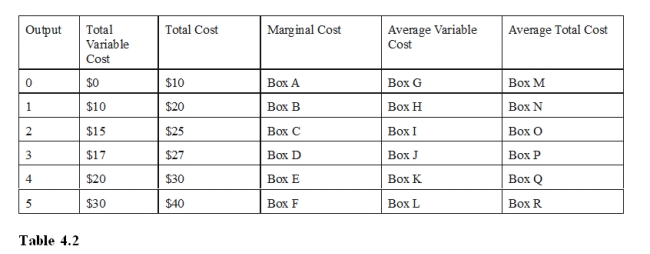

-Refer to Table 4.2, Box K should be filled with

Definitions:

Equilibrium Quantity

The quantity of goods or services that is supplied and demanded at the equilibrium price, where demand equals supply.

Decrease in Price

A reduction in the cost at which goods or services are sold, often leading to increased demand.

Increase in Quantity

A rise in the amount of goods or services produced or supplied.

Market Equilibrium

The state in which market supply and demand balance each other, leading to stable prices.

Q9: If the price of a good decreases

Q29: When estimating GDP using the income approach,

Q46: A per unit tax or percentage tax

Q48: Refer to Table 4.1, Box B should

Q52: Using Figure 1.5 above we know the

Q71: If the total cost of producing 19

Q87: Real Gross Domestic Product is Gross Domestic

Q88: Suppose you can get broadband only from

Q129: If there is an expectation that the

Q201: The equilibrium quantity is<br>A)the amount exchanged at