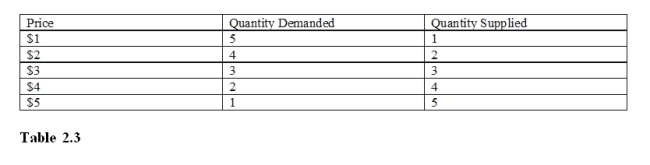

-From Table 2.3, at the price of $1 there is a

Definitions:

Price Floor

A government or regulatory-imposed minimum price for goods or services, intended to prevent prices from dropping too low.

Shortage

A circumstance in which the market desire for a service or product is greater than the supply.

Surplus

The situation in which the quantity supplied of a product exceeds the quantity demanded, often leading to price decreases.

Price Ceiling

A government-imposed limit on how high a price can be charged for a product or service, intended to protect consumers.

Q30: If the price of a good decreases

Q33: The 2001 terrorist attack reduced U.S. aggregate

Q64: Average Total Cost is<br>A)the addition to cost

Q66: In the production of corn, millions of

Q77: Predict the number of unpaired electrons in

Q88: Refer to Table 4.2, Box R should

Q111: If the price of a typical good

Q127: The quintessential example for the price of

Q146: In order to be drawn correctly the

Q202: The decrease in the price of a