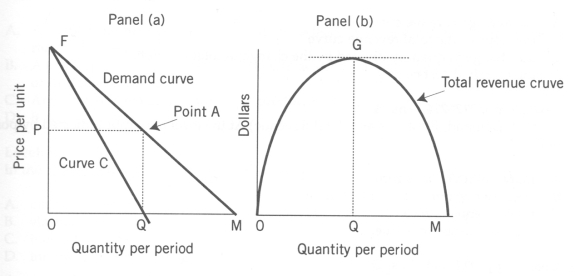

Use the following to answer question(s) : Demand, Elasticity, and Total Revenue

-(Exhibit: Demand, Elasticity, and Total Revenue) If price is lower than P, an increase in price (but not above P) will result in:

Definitions:

Long-Run Equilibrium

A state in economics where all factors of production and costs are variable, leading to a situation where firms are earning normal profits and no new firms enter or exit the industry.

Plaster

A building material used for coating, protecting, and decorating walls and ceilings, made from lime, sand, and water.

Labor

The involvement of human physical exertion and cognitive efforts in the manufacture of goods and services.

Interest Rate

The percentage charged on borrowed money or paid on invested capital, representing the cost of borrowing or the gain on investing.

Q15: Imperfect competition includes:<br>A) monopolistic competition and oligopoly.<br>B)

Q59: In terms of labor supply, the substitution

Q66: If a consumer is buying two goods

Q73: Economists assume that consumers behave in a

Q100: In perfect competition, price will _ marginal

Q106: Firms are organizations that produce goods and

Q128: The HHI is found by squaring the

Q152: (Exhibit: Computing Monopoly Profit) In order to

Q170: According to the utility model of consumer

Q206: At 125,000 units of output, a firm's