Use the following for questions 43-51.

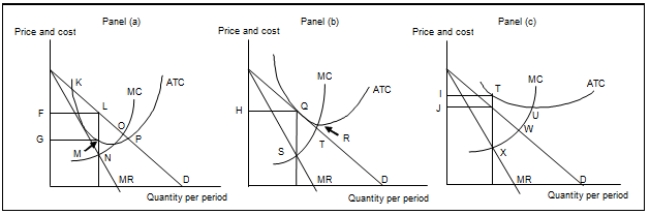

Exhibit: Firms in Monopolistic Competition

-(Exhibit: Firms in Monopolistic Competition) Long-run equilibrium is illustrated at the profit-maximizing price _______ in Panel _______ .

Definitions:

Manufacturing Overhead

All manufacturing costs incurred during the production process that cannot be directly attributed to specific units produced, such as utilities, maintenance, and factory supplies.

Total Variable Cost

The total of variable costs involved in the production of goods or services, which change in proportion to the level of production or activity.

Total Fixed Cost

The sum of all costs required to produce any product or service, which remain unchanged regardless of the company's level of production or output.

Average Variable Cost

The cost that varies with the level of output, divided by the total quantity of output produced, reflecting the average cost per unit of variable expenses.

Q3: (Exhibit: Wage Determination in Perfect Competition) An

Q5: Profit-maximizing firms seek to maximize output.

Q9: The costs incurred by a firm in

Q18: (Exhibit: Monopoly Through Collusion) Given the duopoly

Q55: A change in the quantity demanded of

Q60: (Exhibit: Marginal Revenue Product and Demand) If

Q85: The slope of the total product curve

Q126: Marginal product, mathematically, is the slope of

Q184: (Exhibit: Marginal Revenue Product and Demand) Assume

Q189: In oligopoly, a firm must realize:<br>A) that