Use the following to answer question(s) :

Exhibit: Marginal Decision Rule

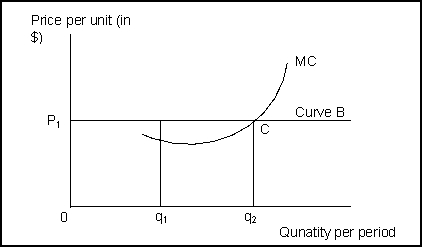

-(Exhibit: Marginal Decision Rule) Economic profit:

Definitions:

Marginal Product

The increase in output resulting from a one-unit increase in the quantity of a particular input, holding other inputs constant.

Isoquants

Isoquants are curves that represent combinations of various inputs that produce the same level of output, used in production theory to analyze input choices.

Input Prices

The cost of resources used in the production of goods and services.

MRTS

Marginal Rate of Technical Substitution, the rate at which one factor must decrease as another increases to keep output constant.

Q2: (Exhibit: Bicycles and Radishes 2) In the

Q42: Changes in the distribution of income in

Q49: A perfectly competitive firm will stay in

Q83: An advantage of marketable pollution permits is

Q110: Perfect competition is characterized by:<br>A) rivalry in

Q112: Gary Becker concluded that discrimination occurs because

Q124: (Exhibit: Production Possibilities Curve 1) If the

Q144: If firms are experiencing economic losses in

Q152: In a market capitalist economy:<br>A) markets are

Q157: A decrease in production costs for firms