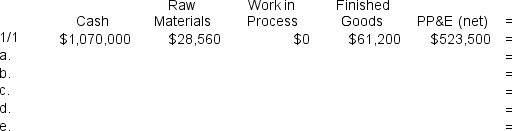

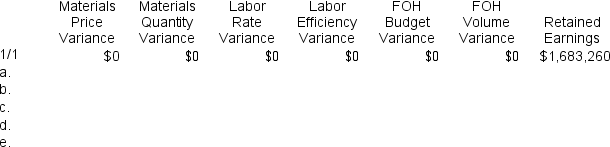

Phann Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead. The standard cost card for the company's only product is as follows:

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $90,000 and budgeted activity of 7,500 hours.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $90,000 and budgeted activity of 7,500 hours.

During the year, the company completed the following transactions:

a. Purchased 59,000 kilos of raw material at a price of $9.20 per kilo.

b. Used 51,340 kilos of the raw material to produce 18,300 units of work in process.

c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 8,850 hours at an average cost of $23.70 per hour.

d. Applied fixed overhead to the 18,300 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $79,400. Of this total, $22,400 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $57,000 related to depreciation of manufacturing equipment.

e. Completed and transferred 18,300 units from work in process to finished goods.

Assume that all transactions are recorded on the below worksheet, which is similar to the worksheet shown in your text except that it has been divided into two parts so that it fits on one page. The beginning balances in each of the accounts have been given. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

-When recording the direct labor costs in transaction (c) above,the Cash account will increase (decrease) by:

Definitions:

Q62: When recording the raw materials purchases in

Q65: Platko Corporation manufactures one product.It does not

Q66: Poorly trained workers could have an unfavorable

Q94: The fixed manufacturing overhead applied to products

Q95: The net operating income in the flexible

Q130: The variable component of the predetermined overhead

Q164: The selling and administrative expense in the

Q179: If the company pursues the investment opportunity

Q200: The administrative expenses in the planning budget

Q210: The activity variance for materials and supplies