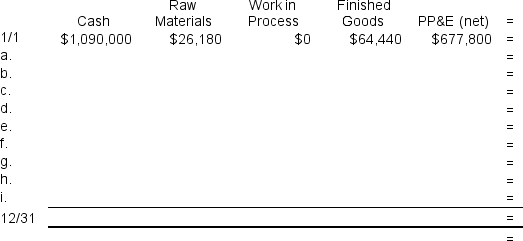

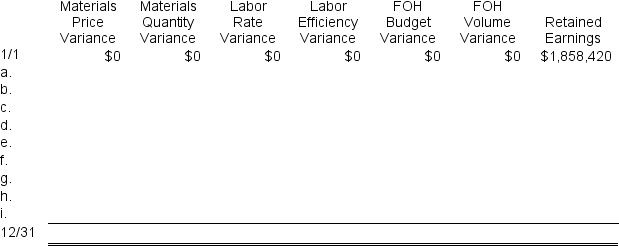

Alvino Corporation manufactures one product. It does not maintain any beginning or ending Work in Process inventories. The company uses a standard cost system in which inventories are recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There is no variable manufacturing overhead.

The standard cost card for the company's only product is as follows:

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $70,000 and budgeted activity of 14,000 hours.

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing overhead of $70,000 and budgeted activity of 14,000 hours.

During the year, the company completed the following transactions:

a. Purchased 32,200 kilos of raw material at a price of $7.80 per kilo. The materials price variance was $22,540 F.

b. Used 30,480 kilos of the raw material to produce 27,800 units of work in process. The materials quantity variance was $850 F.

c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash) worked 18,260 hours at an average cost of $20.50 per hour. The direct labor rate variance was $9,130 U. The labor efficiency variance was $24,000 F.

d. Applied fixed overhead to the 27,800 units in work in process inventory using the predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs for the year were $59,500. Of this total, -$22,500 related to items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $82,000 related to depreciation of manufacturing equipment. The fixed manufacturing overhead budget variance was $10,500 F. The fixed manufacturing overhead volume variance was $27,300 F.

e. Completed and transferred 27,800 units from work in process to finished goods.

f. Sold (for cash) 29,000 units to customers at a price of $31.90 per unit.

g. Transferred the standard cost associated with the 29,000 units sold from finished goods to cost of goods sold.

h. Paid $101,000 of selling and administrative expenses.

i. Closed all standard cost variances to cost of goods sold.

To answer the following questions, you will need to record transactions a through i in the worksheet below. This worksheet is similar to the worksheets in your text except that it has been split into two parts to fit on the page. PP&E (net) stands for Property, Plant, and Equipment net of depreciation.

-The ending balance in the Retained Earnings account at the end of the year is closest to:

Definitions:

Adaptive Learning

A teaching method that uses technology to adjust the content, pace, and approach to match the learner's needs.

Social Models

Representations or frameworks used to understand social processes and interactions, guiding perceptions of societal roles and behaviors.

Vicarious Reinforcement

It occurs when the likelihood of an observer performing a particular behavior increases after they've seen someone else rewarded for that behavior.

Prosocial Behavior

Actions intended to benefit others, including behaviors like helping, sharing, and comforting.

Q8: Macumber Corporation has two operating divisions--an Atlantic

Q61: An unfavorable materials quantity variance occurs when

Q84: What is the maximum price that the

Q91: Nanke Products,Inc.,has a Sensor Division that manufactures

Q122: Brister Incorporated has provided the following data

Q149: Pattison Corporation is a service company that

Q169: Diehl Corporation uses a standard cost system

Q195: The direct labor in the planning budget

Q244: Lido Company's standard and actual costs per

Q329: The occupancy expenses in the flexible budget