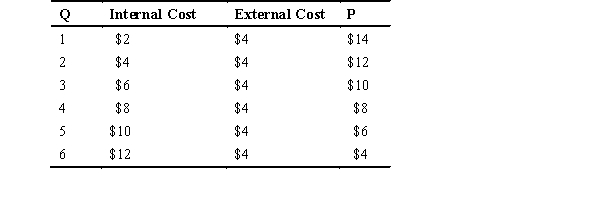

Refer to the accompanying table,where Q represents the quantity produced,internal cost and external cost are given for various quantities,and P represents the price consumers are willing to pay for various quantities to answer the following questions.

-The market equilibrium occurs where price is __________ and quantity is _________.

Definitions:

Output

In economics, output refers to the total amount of goods and services produced by a company, sector, or economy within a certain period of time.

Function

A relation between a set of inputs and a set of permissible outputs, specifying a single output for each input.

Production Function

An equation that describes the relationship between the quantities of productive factors used and the amount of product obtained.

Returns To Scale

Describes how the output of a production process changes as all inputs are scaled up or down by the same proportion.

Q41: Which of the following is NOT an

Q62: A firm's willingness to supply its product

Q63: Price gouging laws will usually result in

Q91: What is the total amount of producer

Q115: Signals<br>A) have no importance in economics.<br>B) convey

Q134: Because of market forces,firms have _ when

Q144: It is important for a firm to

Q151: Why would most economists (and all free-market

Q157: The third-party problem<br>A) occurs when a market

Q166: Use a figure with intersecting supply and