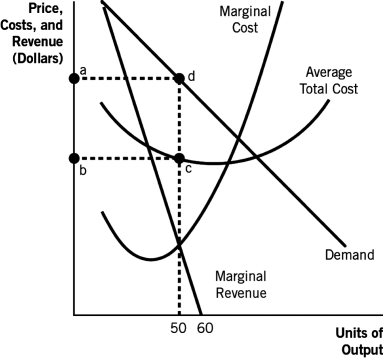

Refer to the following graph to answer the following questions:

-The short-run equilibrium for a monopolistically competitive firm is at price equals $29,average total cost equals $22,and marginal cost equals marginal revenue equals $18.Which of the following is true?

Definitions:

Equilibrium Wage

The wage rate at which the quantity of labor demanded by employers equals the quantity of labor supplied by workers, resulting in no labor surplus or shortage.

Immigrate

To immigrate means to move into a country from another one to live permanently.

Minnesota

A state in the Midwestern United States known for its lakes, forests, and vibrant cultural scene, as well as its contributions to industry, agriculture, and education.

Opportunity Cost

The cost of forgoing the next best alternative when making a decision or choosing one option over another.

Q9: If the price of output is $5,the

Q40: An employee gains work experience by staying

Q76: Assume that two firms (Firm A and

Q85: When teams are able to change ticket

Q87: Refer to the following table.In the Nash

Q93: What theory would lead someone to be

Q108: The _ Act was passed in 1890,and

Q128: The first federal law to place limits

Q145: When a particular strategy produces a better

Q150: The following payoff matrix depicts the possible