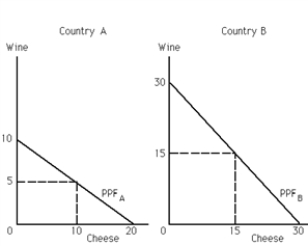

-Refer to Exhibit 34-6.Which of the following terms of trade would both countries agree on?

Definitions:

Long-run Equilibrium

The state in which all factors of production and costs are variable, and firms make neither excess profit nor losses, indicating stability in the market.

Perfectly Competitive

A market structure characterized by many buyers and sellers, homogeneous products, free entry and exit, and perfect information, resulting in firms being price takers.

Price

The amount of money required to purchase a good or service; the value that must be exchanged to acquire a specific product.

Short-run Industry Supply

The total quantity of goods that producers in an industry are willing and able to sell at different prices in a short period, without changing production capacity.

Q2: A score with an extremely high or

Q4: The Real GDP of country X doubled

Q4: The term outsourcing is used to describe

Q7: The foreign exchange market is the market

Q32: Compare a property rights system in which

Q56: Psychologists use frequency tables and histograms to

Q90: Economist A believes that the government spending

Q91: Two economists,A and B,believe that the economy

Q98: "Politics is too often the thing that

Q102: Refer to Exhibit 35-4.Under a fixed exchange