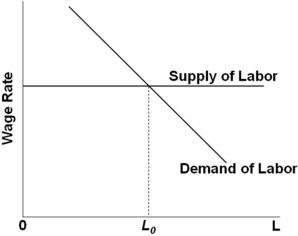

Refer to the above graph.It shows a firm that buys its inputs and sells its output in competitive markets.If the firm develops a new technology that increases labor productivity,the equilibrium level of employment for this firm is expected to be:

Refer to the above graph.It shows a firm that buys its inputs and sells its output in competitive markets.If the firm develops a new technology that increases labor productivity,the equilibrium level of employment for this firm is expected to be:

Definitions:

Minimum Costs

The lowest amount that can be spent on the production of a good or service while maintaining its quality.

Holding Inventory

The process of storing unsold goods or materials that a business intends to sell to generate revenue.

Ordering Costs

Expenses associated with placing orders for goods or services, including cost of paperwork, communication, and transportation.

Just-in-Time Inventory

Just-in-Time Inventory is an inventory management strategy that aims to increase efficiency and decrease waste by receiving goods only as they are needed in the production process.

Q40: Taxes and transfer payments:<br>A) reduce the degree

Q50: Which of the following terms describes a

Q72: In 2009,an unattached individual would be defined

Q77: Mutual interdependence means that each firm in

Q91: The number of countries belonging to the

Q101: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB4893/.jpg" alt=" Refer to the

Q102: The relative efficiency with which a nation

Q105: Under which market model are the conditions

Q125: Which statement concerning monopolistic competition is false?<br>A)

Q162: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB4893/.jpg" alt=" Refer to the