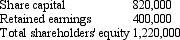

Eagle Ltd is the ultimate parent entity in a group of companies.On 1 July 2003 Eagle Ltd acquired 30 per cent of the issued capital of Sparrow Ltd for a cash consideration of $366,000.At the date of acquisition the net assets of Sparrow Ltd are recorded at fair value and are represented by equity as follows:  Additional information:

Additional information:

During the financial year ending 30 June 2004 Sparrow Ltd makes a profit before tax of $140,000,and an after-tax profit of $89,000.

Sparrow Ltd proposed a dividend of $20,000 for the 2003/2004 period that will be paid early in the next period.

Eagle Ltd does not recognise dividends proposed by associates until they are paid.

During the year ended 30 June 2004 Sparrow made intragroup sales to members of Eagle's economic group.These include:

Sparrow sold inventory to Peregrin Ltd,an 80 per cent owned subsidiary of Eagle Ltd.The inventory cost Sparrow $8,000 and was sold to Peregrin for $12,000.Half of that inventory is still on hand in Peregrin at the end of the period.

Sparrow sold inventory to Seagull Ltd,a 25 per cent owned associate of Eagle's.The inventory cost Sparrow $10,000 and was sold to Seagull for $15,000.Forty per cent of this inventory is still on hand in Seagull at the end of the period.

The tax rate is 30 per cent.

What consolidated journal entry/ies is/are required to equity account for Eagle's interest in Sparrow Ltd for the period ended 30 June 2004?

Definitions:

Import Quota

A government-imposed limit on the quantity or value of goods that can be imported into a country.

Quantity Consumed

The total amount of a good or service that is used or ingested over a specific period of time.

Foreign Exchange

The marketplace for trading currencies, enabling conversion from one currency to another, essential for global trade and investment.

Black Market

An illegal trading environment where goods or services are exchanged in violation of government regulations.

Q2: AAS 25 requires all liabilities of a

Q6: Bonus payments that are part of an

Q7: Intragroup transactions that are to be eliminated

Q8: Large Company owns 80 per cent of

Q15: Non-sequential acquisition is when a parent acquires

Q33: When a joint venturer contributes assets to

Q34: When a parent sells its interest in

Q46: Potential costs of providing segment information include:<br>A)

Q52: On January 1,Year 1,Melon Moving Company paid

Q63: Chico Company experienced an accounting event