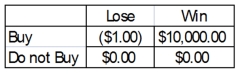

A person is trying to decide if they should buy a lottery ticket. The ticket costs $1.00. If the ticket is a winner, the prize would be $10,000. Knowing that winning $10,000 is not a certain outcome (state of nature), the person finds that the probability of winning is 0.0009. Based on this information, the following payoff table can be constructed.  What is the probability of losing $1.00?

What is the probability of losing $1.00?

Definitions:

Psychotherapy

A form of therapy involving talking with a trained therapist to understand and resolve problematic behaviors, beliefs, feelings, relationship issues, and/or bodily responses.

Validity

The extent to which a test measures or predicts what it is supposed to.

Memory Problems

Difficulties in recalling past events, learning new information, or retaining data, which can vary from mild forgetfulness to severe impairment.

Brilliant Mathematician

An exceptionally talented individual in the field of mathematics, known for their deep understanding and innovative contributions.

Q18: ACFE,the world's largest antifraud organization,requires its members

Q37: To calculate monthly typical seasonal indexes, a

Q39: Which of the following is considered to

Q40: The following linear trend equation was developed

Q40: Which of the following is a key

Q44: Prices and the number produced for selected

Q45: Define autocorrelation.

Q50: Why should any potential conflicts of interest

Q79: The national sales manager for "I colored

Q118: In an acceptance sampling plan, the incoming