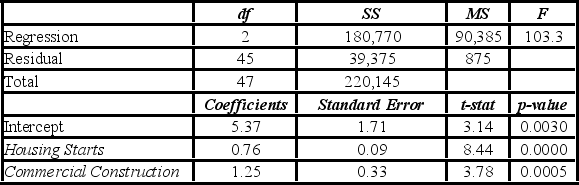

Assume you ran a multiple regression to gain a better understanding of the relationship between lumber sales, housing starts, and commercial construction. The regression uses lumber sales (in $100,000s) as the response variable with housing starts (in 1,000s) and commercial construction (in 1,000s) as the explanatory variables. The estimated model is Lumber Sales = β0 + β1Housing Starts + β2Commercial Constructions + ε. The following ANOVA table summarizes a portion of the regression results.  The standard deviation of the difference between actual lumber sales and the estimate of those sales is ________.

The standard deviation of the difference between actual lumber sales and the estimate of those sales is ________.

Definitions:

Price

is the amount of money required to purchase a good or service, serving as the exchange rate between money and the good or service.

Quantity Supplied

Quantity Supplied refers to the amount of a good or service that producers are willing and able to sell at a given price.

Market Equilibrium

Occurs when the quantity of goods demanded by consumers equals the quantity of goods supplied by producers, resulting in a stable market price.

Price

The amount of money required to purchase a good or service, typically determined by supply and demand.

Q18: Consider the following sample data. <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB6618/.jpg"

Q20: The logit model can be estimated with

Q30: Which of the following types of trend

Q33: In a simple linear regression based on

Q59: A bank manager is interested in assigning

Q61: The test statistic for a test of

Q64: For the exponential model ln(y) = β<sub>0</sub>

Q84: To avoid the dummy variable _, the

Q106: For the log-log model ln(y) = β<sub>0</sub>

Q111: Variables employed in a regression model can