The following are key terms in Chapter 2 that relate to principles of accounting and financial reporting for state and local governments:

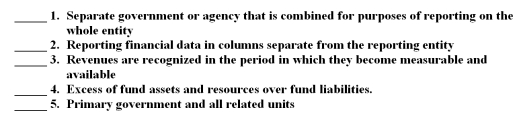

A.Fund equity

B.Modified accrual basis

C.Reporting entity

D.Discrete presentation

E.Component unit

F.Accrual basis

G.Blended presentation

H.Governmental activities

For each of the following definitions,indicate the key term from the list above that best matches by placing the appropriate letter in the blank space next to the definition.

Definitions:

Office Building

A structure designed primarily for the purpose of housing offices and businesses, providing a workspace for employees and services for clients.

Assembly Line

A production process that breaks down the manufacture of a good into steps that are completed in a pre-defined sequence, often on a conveyor belt, to increase efficiency.

Opportunity Cost

The neglect of possible enhancements from other avenues when one direction is pursued.

Capacity Utilization Rate

The capacity utilization rate measures the proportion of potential economic output that is actually realized, often used in manufacturing to indicate the percentage of total productive capacity being utilized.

Q11: Which of the following accounts would least

Q16: Which of the following information should be

Q17: Generally accepted accounting principles applicable to state

Q20: Under GASB reporting entity standards,a component unit

Q21: If general capital assets are being acquired

Q27: To establish a new internal service fund

Q31: Which of the following fund types uses

Q49: Health care organizations often collaborate and combine

Q69: Utility enterprise funds that report to regulatory

Q77: Which of the following financial statement(s)reports both