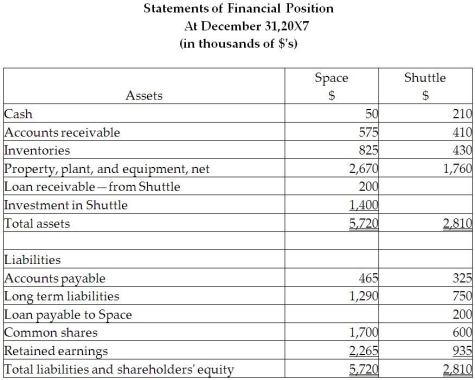

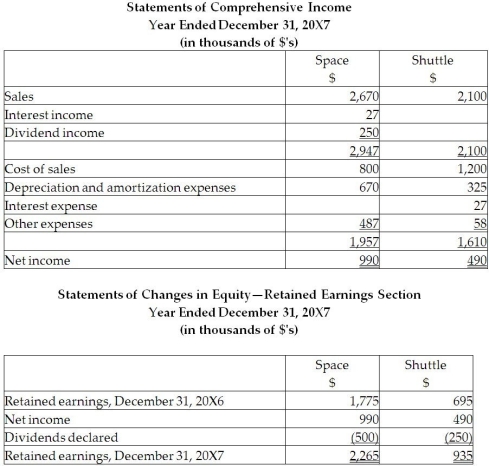

On December 31, 20X5, Space Co. purchased 100% of the outstanding common shares of Shuttle Ltd. for $1,200,000 in shares and $200,000 in cash. The statements of financial position of Space and Shuttle immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

The difference in the carrying value and the fair value of the capital assets for Shuttle relates to its office building. This building was originally purchased by Shuttle in January 20X1 and is being depreciated over 30 years.

During 20X6, the year following the acquisition, the following occurred:

1. Shuttle borrowed $350,000 from Space on June 1, 20X6, and was charged interest at 10% per annum, which it paid on a monthly basis. There were no repayments of principal made during the remainder of the year.

2. Throughout the year, Space purchased merchandise of $800,000 from Shuttle. Shuttle's gross margin is 35% of selling price. At December 31, 20X6, Shuttle still owed Space $250,000 on this merchandise; 60% of this merchandise was resold by Space prior to December 31, 20X6.

3. Shuttle paid dividends of $250,000 at the end of 20X6 and Space paid dividends of $500,000.

During 20X7, the following occurred:

1. Shuttle paid $150,000 on the loan payable to Space on May 30, 20X7.

2. Throughout the year, Space purchased merchandise of $900,000 from Space. Space's gross margin is 35% of selling price. At December 31, 20X6, Shuttle still owed Space $350,000 on this merchandise; 80% of this merchandise was resold by Shuttle prior to December 31, 20X7.

3. The goodwill was tested and found to be impaired, resulting in an impairment loss of $120,000.

4. Shuttle paid dividends of $250,000 at the end of 20X7 and Space paid dividends of $500,000.

Required:

Required:

Calculate the consolidated retained earnings for Space as at December 31, 20X7.

Prepare the consolidated statement of financial position for the year ended December 31, 20X7, for Space.

Definitions:

Output

Output is the quantity of goods or services produced by a company, industry, or economy within a specified period.

Average Product

The output per unit of input, calculated by dividing total output by the quantity of inputs.

Law of Diminishing Returns

An economic principle stating that as additional units of a factor of production are added to a fixed amount of another factor, the incremental increase in output will eventually decrease.

Thomas Malthus

Thomas Malthus was an 18th-century British economist and demographer, best known for his theory that population growth would outpace agricultural production, leading to widespread poverty and famine.

Q5: _ is the aggregation of many similar

Q6: Under the equity method, the purchase price

Q7: Which ratios measure the degree of risk

Q8: Refer to the table above. Using the

Q12: Consists of the three basic accounting elements:

Q24: How does a government statement of cash

Q29: In 20X8, Mallard sold goods to

Q31: Assume that the transaction qualifies as a

Q38: Refer to the table above. The annual

Q47: A cost unit can be:<br>A)a product.<br>B)a department.<br>C)a