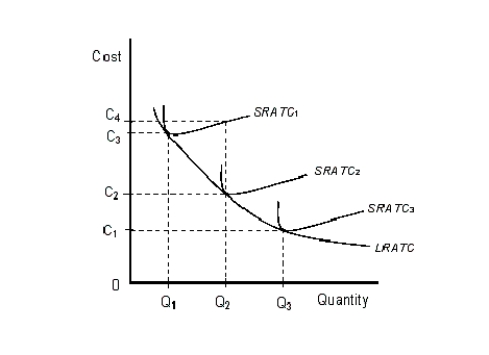

The figure given below shows three Short Run Average Total Cost (SRATC) curves and the Long Run Average Total Cost (LRATC) curve of a firm.Figure 8.3

-If marginal product increases with an increase in the variable input, the marginal cost must also increase as more units of the input are hired.

Definitions:

Availability Of Substitutes

The extent to which similar or alternative products and services are accessible to consumers, influencing their choices and market demand.

Linear Demand

An economic model where demand for a good or service changes proportionately with changes in price.

Unit Elastic

A situation in demand or supply where the elasticity is exactly one, indicating that a change in price results in a proportionate change in the quantity demanded or supplied.

Total Revenue

The total amount of money received by a firm from selling its goods or services.

Q25: "As I add more workers to the

Q35: The opportunity cost of capital is:<br>A)the cost

Q41: Since only a few firms dominate the

Q47: Collusion of firms is legal in the

Q54: Under an oligopoly market structure, rival firms

Q65: If = -1.50 for a good, and

Q66: Refer to Table 11.4. Assuming that the

Q82: A firm will always maximize profit at

Q92: As one moves downward on an indifference

Q113: Under imperfect competition, a firm's:<br>A)demand curve lies