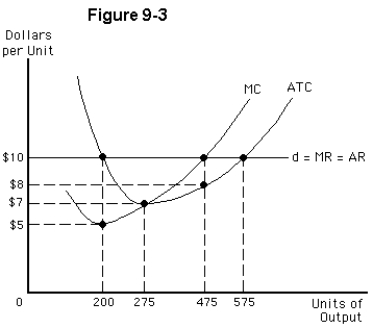

-In short-run equilibrium,the perfectly competitive firm of Figure 9-3 will charge

Definitions:

Elastic

Elastic refers to the responsiveness of the quantity demanded or supplied of a good or service to a change in its price, with high elasticity meaning significant responsiveness.

Average Variable Cost

The cost variable per unit of output produced, calculated by dividing total variable costs by the quantity of output.

Economic Losses

The reduction in financial wealth, goods, or services that results from an event or decision.

Long Run Market Supply Curve

A curve showing the relationship between the price of a good and its supply over a longer period, when all input factors can be varied.

Q40: Both marginal revenue and marginal revenue product

Q45: If marginal utility from consuming an extra

Q47: Monopolies differ from perfectly competitive firms in

Q60: Which of the following determines the maximum

Q75: The demand curve facing a firm shows

Q82: Which of the following statements is true

Q101: Marginal revenue is defined as the<br>A) total

Q106: Whenever marginal cost exceeds marginal revenue,<br>A) profit

Q139: If all consumers satisfy economists' assumptions regarding

Q150: Which of the following formulas represents