Exhibit 14-2

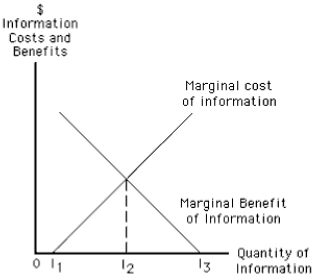

-In Exhibit 14-2, the point I1 indicates

Definitions:

Time To Adjust

This term refers to the period required for changes in economic or policy conditions to take effect in the market or economy.

Price Change

The variation in the selling price of goods and services over a period of time, influenced by factors such as supply and demand, production costs, and market competition.

Inelastic Supply

describes a situation where the quantity supplied of a good is not significantly affected by changes in price.

Quantity Supplied

The total amount of a product that producers are willing and able to sell at a given price over a specified period.

Q3: Which of the following is an example

Q10: A large inheritance from a relative will

Q22: As concentration in an industry increases,the value

Q36: Which of the following is not an

Q51: Which of the following would lead a

Q75: Which of the following could explain an

Q93: The rail system in Metropolis is a

Q95: According to the U.S.Supreme Court's 1920 ruling

Q120: A regulated natural monopoly that must set

Q164: A monopoly is likely to charge a