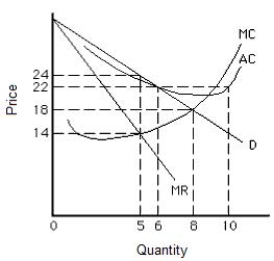

The figure below shows the cost and revenue curves for a natural monopolist. Suppose the monopolist was originally producing at a profit-maximizing output level. If regulators set price equal to marginal cost, the price will change from:

Figure 15.1

Definitions:

Marginal Cost

The increase in cost that comes from making one more unit of a product or service.

Equilibrium Price

The price at which the quantity of a good or service demanded by consumers equals the quantity supplied by producers, leading to a balance in the market.

Equilibrium Quantity

The quantity of goods or services supplied and demanded at the equilibrium price, where market supply equals demand.

Collusion

A secret or illegal cooperation or conspiracy, especially between parties to cheat or deceive others, commonly in the context of firms agreeing on prices or market shares.

Q4: The figure given below shows the marginal

Q8: By requiring that applicants for insurance policies

Q29: Which of the following problems is most

Q55: An ideal example of a vertically integrated

Q64: Eligibility for income assistance benefits requires a

Q70: Control of water pollution from pesticide runoff

Q70: According to Stigler's search model, the marginal

Q75: An externality is:<br>A)a cost of a transaction

Q99: The winner's curse is more likely to

Q114: Intellectual property:<br>A)requires copyright protection that is expensive