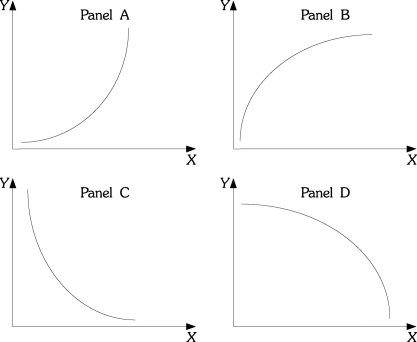

Refer to the information provided in Figure 1.5 below to answer the questions that follow.  Figure 1.5

Figure 1.5

-Refer to Figure 1.5. In many industries, as firms produce additional units, average costs of production decline as the firm produces an additional unit, but average costs declines by a smaller and smaller amount as production continues to increase. If output is graphed on the horizontal axis and average costs are graphed on the vertical axis, the relationship between average costs and output would be like which of the following panels?

Definitions:

Income

Earnings acquired on a consistent basis through employment or investments.

Quantity Demanded

The total amount of a good or service that consumers are willing and able to purchase at a given price within a specific time period.

Quantity Supplied

The amount of a good or service that producers are willing and able to sell at a specific price, over a specified period of time.

Equilibrium

A state in which market supply and demand balance each other, and as a result, prices become stable.

Q2: Which of the following statements is false?<br>A)Each

Q7: The criterion introduced by the Supreme Court

Q19: When one market reaches a new equilibrium,

Q19: Collectors static method groupingBy with two arguments

Q24: When a thread executing a synchronized statement

Q35: Residential structures and inventories are examples of

Q55: ʺDemand determinedʺ means that price is set

Q94: The whole class of goods that will

Q107: The present discounted value of a stream

Q178: A monopolist who has a horizontal ATC