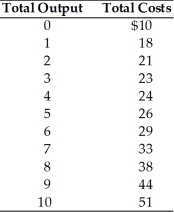

-In the above table, the marginal cost of the fourth unit is

Definitions:

Industry Expansion

The process of an industry growing in size, output, or number of participants, often through increased demand or technological advancements.

Decreasing-Cost Industry

An industry where the average cost of production decreases as the industry grows and output increases, often due to economies of scale.

Demand Occurs

The moment at which consumers are willing and able to purchase a good or service at a given price.

Long-Run Equilibrium

A state in which all factors of production and costs are variable, and firms in the industry are earning only normal profits, with no incentive for entry or exit.

Q52: Which of the following best describes a

Q152: Which of the following is TRUE for

Q153: Suppose Jon Stewart of the "Daily Show"

Q157: Suppose a perfectly competitive firm can produce

Q186: Total fixed cost is<br>A) the cost of

Q197: Suppose the perfectly competitive equilibrium occurs such

Q268: If firms in a perfectly competitive industry

Q302: A disadvantage of the proprietorship form of

Q340: In the short run, the perfectly competitive

Q363: If in the short run total product