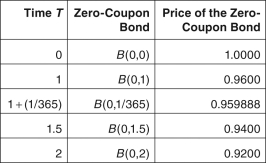

Zero-coupon bond prices are given by B(0,T ) ,where 0 is today,and T (measured in years) is the bond's maturity date.

-Considering the time interval from 1 year to 1.5 years,the simple forward rate is given by:

Definitions:

Independent Variable

The experimental variable used to divide participants into groups.

Interaction

The process by which entities or individuals act upon or communicate with each other.

Dependent Variable

The variable in an experiment that is measured or observed to assess the effect of the independent variable.

Leisure Activities

Activities engaged in for relaxation, enjoyment, or entertainment during free time.

Q7: Suppose that a futures trader has an

Q9: Suppose that you find that YBM's October

Q13: An airlines company is unlikely to use

Q13: If the stock pays a 1 percent

Q13: Which assumption(s)does the reduced-form model relax in

Q14: Consider a newly issued three-year swap receiving

Q14: Expecting freedom from slavery near the end

Q17: Which of the following statement is FALSE

Q31: How did Democrats hope to win the

Q70: Foreign Miners' Tax<br>A)Lands taken by the United