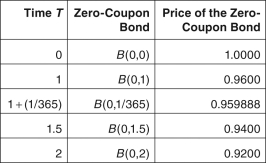

Zero-coupon bond prices are given by B(0,T ) ,where 0 is today,and T (measured in years) is the bond's maturity date.

-Suppose that you compute the simple forward rate over the time period that begins after one year and continues over the next day,and use it as an approximation to the continuously compounded forward rate.Then the value that you obtain is:

Definitions:

Wages

Wages are payments made to employees for their labor or services, typically calculated on an hourly, daily, or piecework basis.

Factors of Production

The inputs used in the production of goods or services in the process of creating economic value; these typically include land, labor, capital, and entrepreneurship.

Monopsony Firm

A market situation where there is only one buyer or a dominant buyer for a product or service, giving that buyer substantial control over market prices and terms.

Competitive Firm

A business that operates in a market with many buyers and sellers, where no single entity can significantly influence the market price of goods and services.

Q3: A stop-loss order (or a sell stop

Q8: In a delta- and gamma-hedged call

Q11: Which of the following is NOT true

Q12: What is the caplet's value?<br>A) 0.000717<br>B) 0.005433<br>C)

Q13: COMIND index is computed by averaging commodity

Q21: Consider the following exotic option whose payoff

Q26: Compare and contrast the rural communalism and

Q67: In its campaign to end slavery,the American

Q74: On July 4,1861,in a statement to a

Q76: For this question,refer to the following two