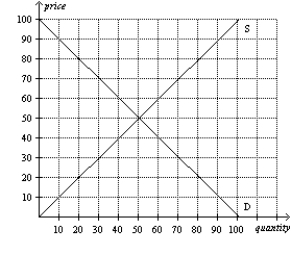

Figure 6-35

-Refer to Figure 6-35.A price ceiling set at $30 would create a shortage of 20 units.

Definitions:

Long-Run Supply Curve

A graphical representation that shows how the quantity supplied of a good changes in response to a price change once producers have had enough time to adjust their production decisions fully.

Constant-Cost Industry

An industry in which costs of production do not change as the industry's output changes.

Decreasing-Cost Industry

An industry where the costs of production decrease as the industry grows and output increases, due to factors such as economies of scale.

Start-Up Firms

New business ventures that are typically tech-focused or innovative in nature, aiming to meet a market need by developing a viable business model.

Q69: Refer to Figure 6-18. The per-unit burden

Q112: Refer to Figure 6-36. If the government

Q125: A price ceiling set below the equilibrium

Q274: If the government passes a law requiring

Q346: Refer to Table 7-10. If there is

Q351: Refer to Table 7-7. You are selling

Q426: Refer to Figure 6-34. If the government

Q450: Refer to Figure 6-35. A price floor

Q467: The goal of the minimum wage is

Q542: Refer to Table 7-7. You have two