Table 24-5

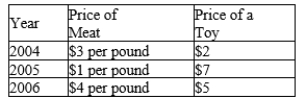

The table below pertains to Wrexington, an economy in which the typical consumer's basket consists of 20 pounds of meat and 10 toys.

-Refer to Table 24-5. The cost of the basket

Definitions:

Variable Cost

Costs that change in proportion to the level of production or sales, such as materials and labor directly involved in manufacturing.

Marginal Cost

The increase in cost resulting from the production of one additional unit of a good or service.

Fixed Input

An input whose quantity is constant and cannot be changed in the short run.

Short Run

A period in economics during which some factors of production are fixed, limiting the ability of a business to fully adjust to market changes.

Q6: Refer to Table 24-12. If the nominal

Q100: Refer to Table 23-4. What was the

Q217: If the quality of a good deteriorates

Q278: In 2009, government purchases was the largest

Q303: Refer to Table 23-11.<br>What was the inflation

Q325: Which of the following changes in the

Q410: The Bureau of Labor Statistics surveys consumers

Q432: Which of the following is correct?<br>A) Over

Q471: Which of the following is included in

Q539: Refer to Table 24-6. If the base