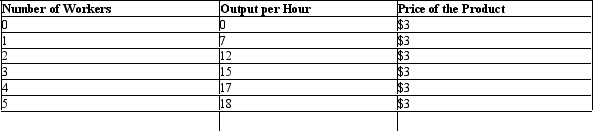

The following table shows output per hour produced by the different units of labor. Table 28.1 The marginal revenue product of a resource is equal to the product of the marginal product of an input and marginal revenue.

The marginal revenue product of a resource is equal to the product of the marginal product of an input and marginal revenue.

According to Table 28.1, the marginal-revenue product of the:

Definitions:

Equilibrium Price

The price at which the quantity of a good demanded by consumers balances the quantity supplied by producers, resulting in a stable market condition.

Suppliers

Businesses or individuals that provide goods or services to another entity, often in exchange for monetary compensation.

Surpluses

Occurs when the quantity supplied of a product exceeds the quantity demanded, often leading to a drop in prices.

Price Up

An increase in the cost of goods or services in the market.

Q18: Which of the following has led to

Q25: The social security system in the United

Q30: Which of the following refers to human

Q40: The high cost of hospital care in

Q48: _ taxes have risen more rapidly in

Q57: Suppose the American Medical Association has been

Q70: The "Robin Hood" tax policy, which taxes

Q71: A Herfindahl index of 5, 000 would

Q91: The following table shows the total output

Q99: Markets can function efficiently only when the