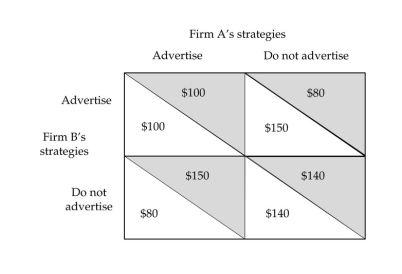

-Two firms are competing in a duopoly and are trying to decide which price to set.The two prices under consideration are a high monopoly price and a low competitive level.If both seller A and seller B chose the monopoly price,each will earn $20 million of economic profit.However,if one picks the monopoly price while the other picks the competitive price,the high-price firm will lose $1 million while the low-price firm will earn $32 million.If both sell at the competitive level,they both earn a normal profit.Complete the payoff matrix below and determine the Nash equilibrium.

Definitions:

Purely Competitive

A market structure characterized by many firms selling identical products, where no single firm can influence the market price.

Monopsonist

A monopsonist is a market condition where there is only one buyer in a market, giving this buyer significant control over the price and terms of purchase.

Labor Supply

The total hours that workers are willing and able to work at a given wage rate, across an economy or market.

Marginal Revenue Product

The additional revenue a firm earns by employing one more unit of input, such as labor or capital.

Q36: Which of the following will increase a

Q75: In which market structure do firms exist

Q105: Regulated natural monopolies can obey a marginal

Q110: A monopolist can make an economic profit

Q146: Babysitting services the oldest son provides his

Q162: "Because firms in an oligopoly are so

Q245: If consumption was 70 percent of GDP

Q266: _ a large number of firms competing

Q302: The above figure shows a motel engaged

Q312: The firm in the above figure has