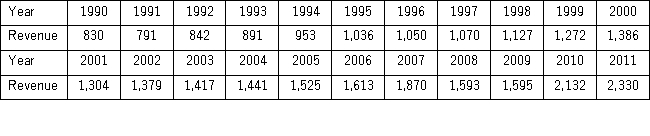

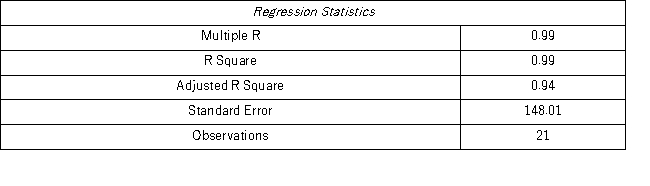

The following table shows the annual revenues (in millions of dollars)of a pharmaceutical company over the period 1990-2011.  The autoregressive models of order 1 and 2,yt = β0 + β1yt - 1 + εt,and yt = β0 + β1yt - 1 + β2yt - 2 + εt,were applied on the time series to make revenue forecasts.The relevant parts of Excel regression outputs are given below.

The autoregressive models of order 1 and 2,yt = β0 + β1yt - 1 + εt,and yt = β0 + β1yt - 1 + β2yt - 2 + εt,were applied on the time series to make revenue forecasts.The relevant parts of Excel regression outputs are given below.

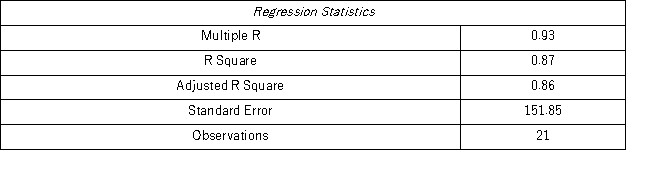

Model AR(1):

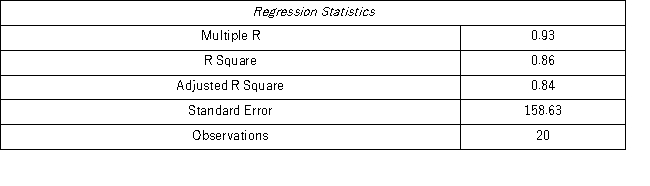

Model AR(2):

Model AR(2):

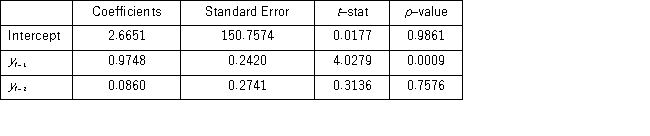

When for AR(1),H0: β0 = 0 is tested against HA: β0 ≠ 0,the p-value of this t test shown by Excel output is 0.9590.This could suggest that the model yt = β1yt-1 + εt might be an alternative to the AR(1)model yt = β0 + β1yt-1 + εt.Excel partial output for this simplified model is as follows:

When for AR(1),H0: β0 = 0 is tested against HA: β0 ≠ 0,the p-value of this t test shown by Excel output is 0.9590.This could suggest that the model yt = β1yt-1 + εt might be an alternative to the AR(1)model yt = β0 + β1yt-1 + εt.Excel partial output for this simplified model is as follows:

(Use Regression in Data Analysis of Excel. )

(Use Regression in Data Analysis of Excel. )

Compare the autoregressive models yt = β0 + β1yt-1 + εt;yt = β0 + β1yt-1 + β2yt-2 + εt,andyt = β1yt-1 + εt,through the use of MSE and MAD.

Definitions:

Primary Socialization

Is the process of acquiring the basic skills needed to function in society during childhood. Primary socialization usually takes place in a family.

School

An educational institution where children and young people receive formal education through a structured curriculum.

Resocialization

The process by which one's sense of social values, beliefs, and norms are re-engineered, often in a new social environment.

Hidden Curriculum

The unintended lessons, values, and perspectives that students learn in school, which are not part of the formal curriculum.

Q23: Consider the following regression results based on

Q46: A sociologist wishes to study the relationship

Q70: A bank manager is interested in assigning

Q72: The following table shows the value of

Q86: The following Excel scatterplot with the fitted

Q94: A dummy variable is also referred to

Q113: The major shortcoming of the general linear

Q115: The linear trend, <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB4266/.jpg" alt="The linear

Q119: A real estate analyst believes that the

Q127: An real estate analyst believes that the