(Requires Appendix material)Your textbook states that in "the distributed lag regression model,the error term ut can be correlated with its lagged values.This autocorrelation arises,because,in time series data,the omitted factors that comprise ut can themselves be serially correlated."

(a)Give an example what the authors have in mind.

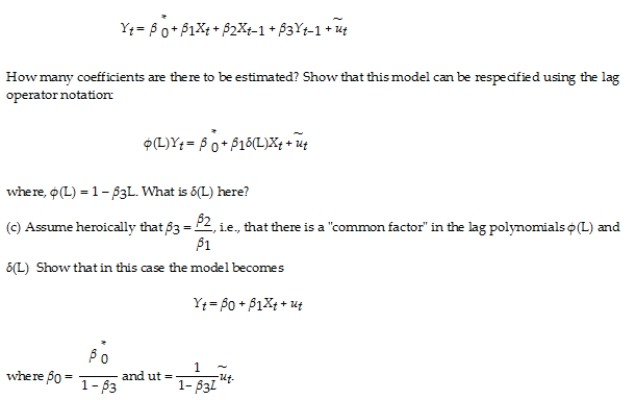

(b)Consider the ADL model,where the X's are strictly exogenous,and there is no autocorrelation (and/or heteroskedasticity)in the error term.  (d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

(d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

Definitions:

Q5: In the binary dependent variable model,a predicted

Q9: One of the properties of the OLS

Q14: Consider the following model<br>Yt = α0 +

Q34: The following is not part of the

Q43: In the case when the errors are

Q44: The interpretation of the coefficients in a

Q57: (Requires Appendix)The sample regression line estimated by

Q61: A 99% confidence interval is wider than

Q62: A simple random sample of 100 college

Q87: A noted psychic was tested for extrasensory