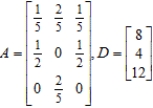

Matrix A is an input-output matrix associated with an economy, and matrix D (units in millions of dollars) is a demand vector. Find the final outputs of each industry so that the demands of both industry and the open sector are met.

Definitions:

Equilibrium Price

The price at which the quantity of a good demanded by consumers equals the quantity supplied by producers, leading to a state of market equilibrium.

Equilibrium Price

The cost at which the amount of a product that buyers want to purchase matches the amount that sellers are willing to supply, creating equilibrium in the market.

Marginal Cost

Marginal cost is the increase in total cost that arises from producing one additional unit of a product or service.

Total Variable Costs

The sum of all costs that vary directly with the level of production, such as materials and labor directly involved in the production process.

Q12: Deluxe River Cruises operates a fleet of

Q16: Rainbow Harbor Cruises charges $8/adult and $4/child

Q22: Which statement about type 1 diabetes is

Q27: Cementoma is a term once used for

Q83: Find an equation of the line that

Q118: Refer to the accompanying figure and determine

Q149: An office building worth $1 million when

Q189: Determine graphically the solution set for the

Q227: Find the transpose of the matrix. <img

Q261: Determine whether the system of linear equations