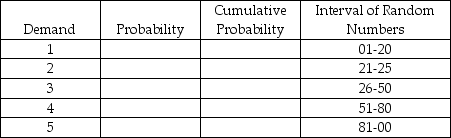

Complete the following table in preparation for a Monte Carlo simulation.

Definitions:

Marginal Product

The additional output that is produced by employing one more unit of a particular input, while holding other inputs constant.

Fixed Cost

A financial outlay that is unaffected by variations in the production or sales levels of goods and services.

Marginal Cost

The expense associated with creating an extra unit of a product or service.

Total Cost

The complete cost of producing a specific quantity of output, including both fixed and variable costs.

Q7: The three information needs of a transportation

Q36: A manufacturer of semiconductor "wafers" has been

Q40: When the number of shipments in a

Q53: Identify the seven steps involved in using

Q54: Identify the seven major measures of a

Q67: Three critical path activities are candidates for

Q68: What does the stepping-stone method do?

Q83: A financial advisor is about to build

Q86: A transportation problem with 8 sources and

Q135: Which of the following is least likely