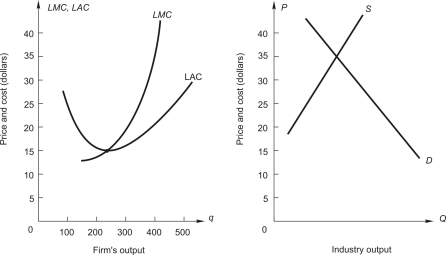

Below,the graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry.The graph on the right shows demand and long-run supply for an increasing-cost industry.  If this were an increasing cost industry,what would be the price when the industry gets to long-run competitive equilibrium?

If this were an increasing cost industry,what would be the price when the industry gets to long-run competitive equilibrium?

Definitions:

Objects into Containers

The process or action of placing things inside receptacles for storage, transport, or organization.

Pincer Grasp

A developmental milestone in which a child uses the thumb and forefinger to pick up small objects, reflecting fine motor skill development.

Baby Bottle

A container with a nipple to drink directly from, used for feeding babies and young children with milk, formula, or other liquids.

Rattle

A toy designed for infants and toddlers that produces sound when shaken, aiding in sensory development and motor skills.

Q19: The following linear demand specification is estimated

Q21: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2562/.jpg" alt=" In the table

Q21: A price-setting firm faces the following estimated

Q23: A consulting firm estimates the following quarterly

Q31: A radio manufacturer has two plants --

Q45: Which of the following represents a short-run

Q48: The empirical specification <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB2562/.jpg" alt="The empirical

Q52: To answer the question,refer to the following

Q55: You overhear a businessman say: "We want

Q56: A sofa manufacturer currently is using 50