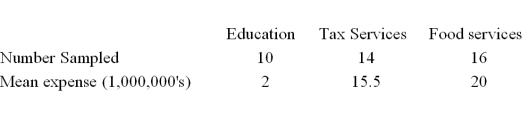

A random sample of 40 companies with assets over $10 million was selected and asked for their annual computer technology expense and industry.The ANOVA comparing the average computer technology expense among three industries rejected the null hypothesis.The Mean Square Error (MSE) was 195.The following table summarized the results:  Based on the comparison between the mean computer technology expense for companies in the Tax Service and Food Service industries,the 95% confidence interval shows an interval of -14.85 to 5.85 for the difference.This result indicates that

Based on the comparison between the mean computer technology expense for companies in the Tax Service and Food Service industries,the 95% confidence interval shows an interval of -14.85 to 5.85 for the difference.This result indicates that

Definitions:

Average Cost Formula

A method used to calculate the cost of goods sold and ending inventory by taking the total cost of goods available for sale and dividing it by the total number of units available for sale.

Cost of Goods Sold

The cost of goods sold (COGS) refers to the direct costs attributable to the production of the goods sold by a company, including material and labor costs.

Specific Identification

An inventory valuation method where each item in inventory is matched with a specific cost.

Inventory Costing

Inventory costing is the method used to assign costs to inventory items, determining the cost of goods sold and remaining inventory value.

Q1: In stratified random sampling,a population is divided

Q10: If the hypothesis,H<sub>o</sub>: <span class="ql-formula"

Q14: The F-distribution is useful when testing a

Q31: The t distribution is a continuous distribution.

Q43: As the degrees of freedom increase,the shape

Q44: When determining how well an observed set

Q49: The proportion of junior executives leaving large

Q74: When conducting a hypothesis test with chi-square

Q78: In an one-way ANOVA,what are the degrees

Q85: Two accounting professors decided to compare the