Use the following to answer questions:

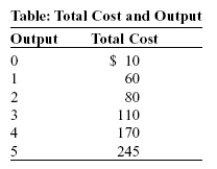

-(Table: Total Cost and Output) Look at the table Total Cost and Output, which describes Sergei's total costs for his perfectly competitive all natural ice cream firm. If there are 100 firms in the all-natural ice cream industry, which of the following is a point on the industry short-run supply curve?

Definitions:

Marginal Cost

The increase in cost that arises from producing one additional unit of a good or service.

Competitive Industry

An industry in which numerous producers supply a homogeneous product or service, leading to competition over price and quality.

Marginal Cost

The extra expenditure needed to manufacture one more unit of a good or service.

Average Cost

The total cost of production divided by the quantity of output produced; it's a measure of how much it costs, on average, to produce one unit of output.

Q22: A perfectly competitive firm is a:<br>A) price

Q51: Children's price elasticity of demand for hot

Q111: (Table: Total Cost and Output) Look at

Q120: If some firms in a perfectly competitive

Q185: (Table: Costs of Birthday Cakes) Look at

Q231: The government can reduce the inefficiency associated

Q245: (Figure: The Total Product) Look at the

Q297: At the long-run quantity of output, where

Q338: (Figure: The Monopolist II) Look at the

Q348: Think about running a restaurant. Probably:<br>A) cooks