Use the following to answer questions .

Exhibit: Demand and Supply of Gasoline

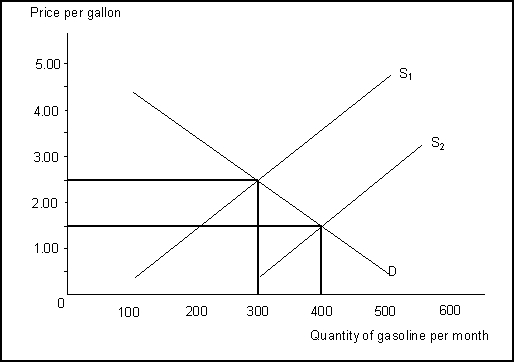

-(Exhibit: Demand and Supply of Gasoline) The initial price and quantity (at intersection of S1 and D) in equilibrium are:

Definitions:

Average Fixed Cost

The fixed costs of production (costs that do not change with the level of output) divided by the quantity of output produced, which decreases as output increases.

Total Product

The total quantity of output produced by a firm during a given time period with a given amount of inputs.

Supply Curve

A graphical representation showing the relationship between the price of a good and the quantity supplied by producers.

Minimum Point

The lowest point on a curve, often referring to the least cost or output level in various economic or mathematical models.

Q8: The gains or benefits from trade are:<br>A)A

Q8: An arrangement in which consumers choose their

Q21: (Exhibit: Circular Flow Model)<br>The exhibit shows a

Q26: Which of the following statements is NOT

Q38: (Exhibit: Demand and Supply-Determinants)<br>The exhibit shows how

Q40: GDP increases if you purchase General Motors

Q51: In the calculation of GDP, the value

Q101: The economic way of thinking includes:<br>A)more attention

Q116: If an economy is producing a combination

Q197: (Exhibit: Demand and Supply Curves)<br>A surplus of