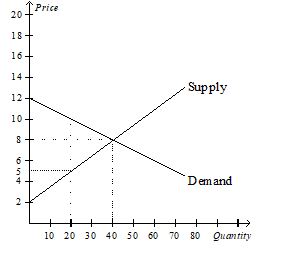

Answer the following questions based on the graph that represents J.R.'s demand for ribs per week at Judy's Rib Shack.

a.At the equilibrium price,how many ribs would J.R.be willing to purchase?

b.How much is J.R.willing to pay for 20 ribs?

c.What is the magnitude of J.R.'s consumer surplus at the equilibrium price?

d.At the equilibrium price,how many ribs would Judy be willing to sell?

e.How high must the price of ribs be for Judy to supply 20 ribs to the market?

f.At the equilibrium price,what is the magnitude of total surplus in the market?

g.If the price of ribs rose to $10,what would happen to J.R.'s consumer surplus?

h.If the price of ribs fell to $5,what would happen to Judy's producer surplus?

i.Explain why the graph that is shown verifies the fact that the market equilibrium (quantity)maximizes the sum of producer and consumer surplus.

Definitions:

Inventory Cost Card

A record-keeping tool that tracks the cost associated with a specific item of inventory, detailing purchases, sales, and adjustments.

Perpetual Inventory System

An inventory management system where updates to inventory records are made in real-time following each sale or purchase transaction.

FIFO

An inventory valuation method that assumes the first items acquired are the first ones sold, standing for First-In, First-Out.

Last-in, First-out

An inventory valuation method where the most recently produced or purchased items are the first to be expensed, often used to manage costs and taxes.

Q7: Refer to Table 7-5.If the market price

Q52: Refer to Figure 8-9.The producer surplus with

Q88: Total surplus measures the<br>A) loss to buyers

Q161: A country has a comparative advantage in

Q165: Refer to Figure 7-13.Suppose the price of

Q234: Refer to Figure 8-10.Suppose the government imposes

Q256: Refer to Figure 8-2.The per-unit burden of

Q302: For any given quantity,the price on a

Q355: Refer to Figure 8-9.The imposition of the

Q359: A drought in California destroys many red