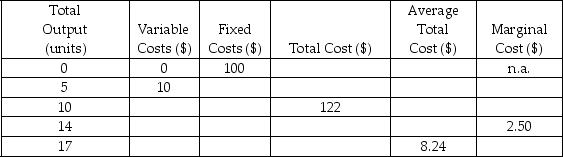

The following table shows the total output, variable costs, fixed costs, total costs, average total costs, and marginal costs of a firm, with some cells in the table intentionally left blank.

-Refer to the table above.What is the total cost of this firm when it doesn't produce any output?

Definitions:

Market Equilibrium

A condition in a market where the quantity demanded equals the quantity supplied, leading to no pressure for price to change.

Minimum Price

The lowest possible price at which a good or service can be sold, often set by legal or regulatory authorities to protect producers or consumers.

Deadweight Loss

A loss of economic efficiency that occurs when the equilibrium for a good or a service is not achieved or is not achievable.

Government Cost

Government cost refers to the expenses incurred by the government in the course of its operations, including public services, defense, infrastructure, and social programs.

Q25: If the quantity of milk is measured

Q82: Refer to the figure above.As firms enter

Q83: If Maylin has $150 of income to

Q100: Refer to the table above.What is the

Q134: A budget constraint is a straight line

Q150: Refer to the scenario above.MLB forecasted that

Q161: Differentiate between the following.<br>a)Normal goods and inferior

Q177: Which statement is consistent with the study

Q236: Refer to the graph above.At the competitive

Q261: A firm's optimal output is 1,000 units