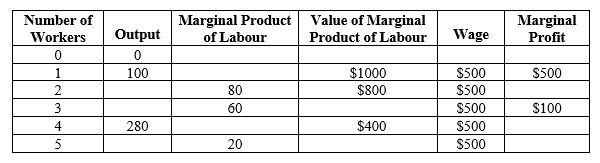

Table 18-1

-Refer to Table 18-1.To maximize its profit,how many workers will the firm hire

Definitions:

Output

The total amount of goods or services produced by a firm, industry, or economy over a specific period.

Average Total Cost

The total cost of production divided by the quantity of output, representing the per-unit cost of production.

Short Run

The short run in economics refers to a period during which at least one input, such as plant size, is fixed and cannot be changed by the firm.

Competitive Firm

A company operating in a market where it has to compete with other firms for consumers, and has no power to set the price of its products, leading to market-driven pricing strategies.

Q10: What effect does diminishing marginal product have

Q50: How is the income distribution in a

Q74: In the short run,a firm in a

Q83: What was discovered in the case study

Q96: Refer to Table 17-2.Assume that there are

Q122: What is the general term for market

Q137: When a monopoly charges a higher price,fewer

Q146: If the price of airline tickets falls,what

Q179: Refer to Scenario 17-3.Parliament passed a law

Q194: Refer to Table 17-4.When this game reaches