Use the figure below to answer the following questions.

Figure 22.3.2

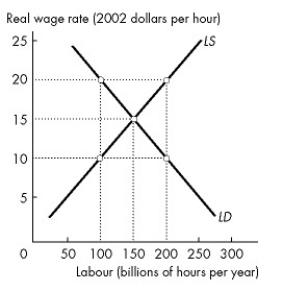

-Refer to Figure 22.3.2. The equilibrium quantity of labour is

Definitions:

Constant-Cost Industry

A constant-cost industry is an industry where the costs of production, including inputs, do not change as the industry's output changes.

Demand Shift

Occurs when the entire demand curve moves due to changes in factors other than the price of the good, such as consumer preferences or income.

Supply Increase

A situation where the quantity of a good or service that is available to consumers rises.

Increasing-Cost Industry

An increasing-cost industry is one in which costs of production increase as the industry expands, often due to factors like limited resources or higher input prices.

Q9: Suppose Mail Boxes Etc.buys a new copier

Q13: Refer to Table 21.3.2.From the data in

Q21: Refer to Figure 22.3.2.The equilibrium quantity of

Q24: Refer to Fact 24.3.2.Based on the Bank

Q26: The business cycle is defined as the<br>A)regular

Q62: Tom takes 20 minutes to cook an

Q67: Frictional unemployment _.<br>A)includes discouraged workers<br>B)is voluntary part-time

Q80: When the real interest rate increases,<br>A)the supply

Q98: At the beginning of the year,your wealth

Q116: Which one of the following would result