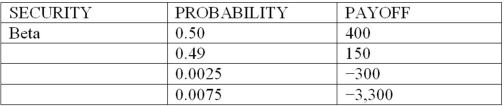

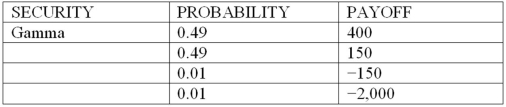

Consider the following discrete probability distributions of payoffs for 3 securities that are held in a DI's trading portfolio (payoff amounts shown are in $millions) :

Based on your answers to the previous three questions, which of the following is true?

Based on your answers to the previous three questions, which of the following is true?

Definitions:

Pay-per-view Movies

A service that allows consumers to pay for individual movies to watch rather than subscribing to a broad service offering.

Common Resource

A resource like air or water that is available to all but can be depleted by overuse.

Nonrival

A characteristic of a good or service indicating that one person's consumption does not diminish the availability of that good for consumption by others.

Market Economy

An economy in which decisions about production and consumption are made by individual producers and consumers.

Q4: Commercial letters of credit are used only

Q6: Which approach used in calculating capital to

Q20: The following three FIs dominate a local

Q26: The following market value balance sheet of

Q46: In international finance, the debt service ratio

Q54: Consider the following discrete probability distributions of

Q66: Performing loans in the LDC debt market

Q67: Under market value accounting methods, FIs<br>A)must write

Q77: Which of the following observations is NOT

Q85: The following information on the mortality rate