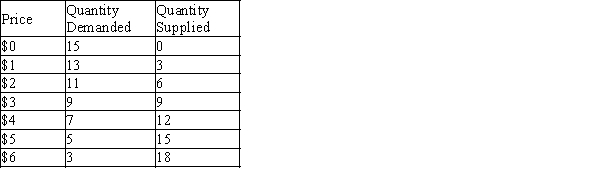

Table 6-4

The following table contains the demand schedule and supply schedule for a market for a particular good. Suppose sellers of the good successfully lobby Congress to impose a price floor $3 above the equilibrium price in this market.

-Refer to Table 6-4. Following the imposition of a price floor $3 above the equilibrium price, irate buyers convince Congress to repeal the price floor and to impose a price ceiling $1 below the former price floor. The resulting shortage is

Definitions:

Long-Run Cost Curve

A graphical representation showing the lowest cost at which any given level of output can be produced in the long run, where all inputs are variable.

Industry Supply Curve

A graph that shows the quantity of goods that producers are willing and able to sell at different price levels in a specific industry.

Marginal Costs

Marginal costs are the additional costs incurred to produce one more unit of a product or service.

Total Cost Function

Describes the complete cost of producing a given level of output, summing up all variable and fixed costs associated with production.

Q112: On a graph,consumer surplus is represented by

Q158: Refer to Figure 5-6.Using the midpoint method,the

Q166: In which of the following situations will

Q169: Markets will always allocate resources efficiently.

Q182: Consumer surplus is the amount a buyer

Q316: Refer to Figure 6-4.Suppose a price ceiling

Q323: Moving downward and to the right along

Q344: Refer to Table 7-6.Who is a marginal

Q356: Refer to Table 7-9.Both the demand curve

Q387: A large majority of economists favor eliminating